Startups with 50 or more full-time employees, including full-time equivalent employees, use IRS Form 1095-C to report information about the health coverage they offer to their employees.

This form is a key component of the Affordable Care Act (ACA) compliance requirements for applicable large employers (ALEs).

Step-by-step instructions: Form 1095-C

IRS Form 1095-C, Employer-Provided Health Insurance Offer and Coverage, is used by applicable large employers (ALEs), typically with 50 or more full-time employees, to report information about health insurance coverage offered to their employees. Like many tax forms, this form can be complex and we strongly recommend that startups consult a tax professional or CPA. This form is part of the Affordable Care Act (ACA) reporting requirements.

Here are step-by-step Form 1095-C instructions for a startup company to fill out this form:

Step 1: Confirm Your Startup’s Filing Requirements

Ensure your startup is required to file Form 1095-C:

-

Your startup is considered an Applicable Large Employer (ALE) if you employed an average of 50 or more full-time employees (or full-time equivalents) during the previous calendar year.

-

You must file Form 1095-C for each full-time employee, even if they did not participate in your health plan.

Step 2: Download Form 1095-C and Instructions

- Visit the IRS website and download the latest version of Form 1095-C and the corresponding Form 1095-C Instructions.

Step 3: Complete Part I - Employee and Employer Information

-

Employee Information (Lines 1-6)

- Line 1: Enter the employee’s full name.

- Line 2: Enter the employee’s Social Security Number (SSN).

- Line 3: Enter the employee’s street address, including city, state, and ZIP code.

-

Employer Information (Lines 7-13)

- Line 7: Enter your startup’s Employer Identification Number (EIN).

- Line 8: Enter your startup’s name (as it appears on tax documents).

- Line 9: Enter your startup’s street address, including city, state, and ZIP code.

- Line 10: Enter a contact phone number for your startup.

- Line 11: Enter your startup’s name again.

- Line 12: Enter your EIN again.

- Line 13: Enter the employer’s address once more (including city, state, and ZIP code).

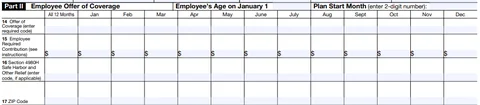

Step 4: Complete Part II - Employee Offer of Coverage

This section reports the offer of health insurance coverage made to the employee during the tax year.

-

Line 14 - Offer of Coverage Code

- Enter the appropriate code for each month in the year to indicate the type of coverage you offered the employee.

-

Example codes:

- Code 1A: Minimum essential coverage providing minimum value offered to full-time employee, with affordable coverage based on the federal poverty line.

- Code 1E: Minimum essential coverage providing minimum value offered to the employee and at least minimum essential coverage offered to dependent(s) and spouse.

- If the offer was made for all 12 months, enter the code in the “All 12 Months” box; otherwise, enter the code in the boxes for each applicable month.

-

Line 15 - Employee Share of Lowest-Cost Monthly Premium

- If Code 1B, 1C, 1D, or 1E was entered in Line 14, enter the employee’s share of the lowest-cost monthly premium for self-only minimum essential coverage that provides minimum value.

- Leave this blank if no offer was made, or if you entered Code 1A in Line 14.

-

Line 16 - Applicable Safe Harbor Codes

- Enter a safe harbor code (if applicable) to explain why your startup may be exempt from a penalty under the employer shared responsibility provisions (IRC Section 4980H).

-

Example codes:

- Code 2A: Employee was not employed during the month.

- Code 2C: Employee enrolled in coverage offered.

- Code 2G: Offer of coverage was affordable based on the federal poverty line.

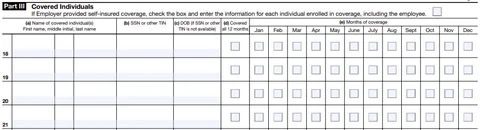

Step 5: Complete Part III - Covered Individuals (if applicable)

This section is completed only if your startup’s health insurance is self-insured. If your startup offers fully insured plans, skip this section.

-

Column (a) - Name of Covered Individual

- List the name of the employee and any covered dependents.

-

Column (b) - SSN

- Enter the Social Security Number for each covered individual. If you do not have an SSN for a dependent, use their date of birth in column (c).

-

Column (c) - Date of Birth

- Enter the date of birth only if the SSN is not available.

-

Column (d) - Covered All 12 Months

- If the individual was covered for the entire year, check this box.

-

Column (e) - Months of Coverage

- If the individual was covered for fewer than 12 months, check the box for each month in which the individual was covered.

Step 6: Review and Prepare for Filing

-

Review. Double-check all employee and employer information for accuracy, especially SSNs and EINs.

-

Corrections. Make sure all the information aligns with the insurance coverage provided throughout the year.

Step 7: File Form 1095-C with the IRS

-

Electronic Filing: If you are filing 250 or more forms, you are required to file electronically through the IRS Affordable Care Act Information Returns (AIR) system.

-

Paper Filing: If you are filing fewer than 250 forms, you can submit them by mail. The address depends on your business location, so check the IRS instructions.

Step 8: Distribute Form 1095-C to Employees

- You must provide a copy of Form 1095-C to each employee by March 2 (or the next business day if March 2 is a weekend or holiday) of the year following the reporting year. This can be done electronically (with employee consent) or by mail.

Step 9: Keep Records

- Retain copies of Form 1095-C and all supporting documentation for at least three years in case of an IRS audit.