Simply keeping millions of dollars in a bank account is clearly no longer a smart cash management strategy for VC backed startups.

But investing the proceeds from a successful VC fundraise is not a trivial task, and establishing – and following – a clear startup investment policy statement is an important step to intelligently handling a company’s cash.

Without guidelines, you can make some very costly mistakes. And part of those guidelines is developing a cash investment policy statement (IPS), which is sometimes referred to as a cash investment plan, or sometimes as a treasury policy statement. Broadly speaking, your IPS is your framework for investing cash you don’t currently need.

It’s important to note up front that startups should NEVER focus on earning returns. Your primary goal is always to protect your funds. In the past, many founders simply put their funds in a bank account, but recent events have demonstrated that may not be the safest option, since FDIC insurance only covers $250,000, and many startups may have millions in venture capital (read more about options to protect larger sums). Startups should focus on cash and low-risk cash equivalents, like short-term US Treasury bonds, and not invest in highly volatile instruments like stocks or stock mutual funds. We’ll cover potential investments in more detail below.

After you create your IPS, have your corporate attorney look it over. Next, your IPS should be approved by your board of directors, and the fact that it’s ratified should be reflected in your board minutes. For founders and CEOs, a firm policy approved by your board protects you from mismanagement, poor decisions, and potential liability. Finally, you’ll also want to share it with the financial institutions that are managing your money. Founders who make serious mistakes or mishandle their cash can bankrupt their startups, and it’s unlikely they’ll be able to obtain venture capital for any future endeavors.

Developing a company’s IPS typically involves looking at the following areas and specifying how you want your cash handled. Startups are different from standard companies and we’ll cover that as we work through the process. Remember that these are just general guidelines and you should consult with your accounting team and financial advisor(s) when drafting your plan.

- Objectives. This includes things like the portfolio’s goals (for example, capital preservation and income), return targets, risk tolerance, and other constraints like time horizon, based on your runway.

- Roles and responsibilities. Who will administer the investment plan?

- Guidelines for investments. This spells out the types of investment vehicles that you’ll allow.

- Asset allocation requirements. Asset allocation refers to the percentage of the overall portfolio that is assigned to different investment options.

- Liquidity. Startups need highly liquid investments that can be sold easily and quickly.

- Maturity. This specifies the length of the investments in your portfolio. Startups can’t afford to have funds tied up in long-term investments.

- Performance. Companies often set a benchmark for the performance of the portfolio, but for startups, performance is never the primary objective. In addition, this section may specify the frequency that investment managers will provide statements of transactions and market valuations.

- Transparency. This outlines the types of accounts in which securities may be held, and also specifies reporting requirements.

As a founder, you should have a detailed understanding of your runway, burn rate, and when you’ll need to seek funding next. The first step in smart cash management is having solid cash burn projections. Consider using one of our free financial model templates if you don’t already have one. Knowing how many months your cash needs to last helps you separate your funds into two categories:

- Operating cash is the money you need to run your business for a set period, like six months.This includes things like salaries, rent, payments to vendors and contractors, and other expenses.

- Strategic cash is the funds you won’t need for a longer period of time, so you have a little more flexibility with this money.

Understanding your projected cash needs is critical to getting the treasury policy right

You do not want to miss payroll or a major vendor payment because your cash was tied up in a bond! Use your projections to establish your cash needs for the next three, six, nine and 12 months. One way to do this is to list out the cash you’ll need for every month, by month, for the next 12 months. Or, some founders like to list out their quarterly cash needs for the next 4 quarters. Here is an example on a quarterly basis:

| Quarter | Months From Now | Quarterly Cash Burn |

|---|---|---|

| Q2 2023 | +3 | $750,000 |

| Q3 2023 | +6 | $850,000 |

| Q4 2023 | +9 | $875,000 |

| Q1 2024 | +12 | $950,000 |

Operating cash needs to be kept in a highly liquid account that you can pull from when you need it. If your company is following the guidance to have 6 months of cash highly liquid, then you’d have $750,000 + $850,000 in cash in a highly liquid account. This might be all in a checking account, or for a startup looking for other low-risk options, some may be in next-day liquid money market accounts, or money market funds, which typically can be converted to cash in three days.

Note: Money market funds should be held in your company’s name with the custodian, not in a bank’s or broker’s name. Another option to protect your funds are networked deposit services, which spread deposits across multiple banks in a network in increments of $250,000, providing greater FDIC protection. These accounts are often called Insured Cash Sweep® or Demand Deposit Marketplace® accounts, and are usually quite liquid – check with your bank to get the details on the specific liquidity features of their products.

Strategic cash can be less liquid, so you may be able to look at opportunities to get a higher yield while still protecting your cash. Having the projected cash needs by quarter or month helps you decide how long you can lock your cash up, and set up investments that become liquid as you need them. Creating the plan on managing your strategic cash is where your investment policy statement comes into play.

Download a sample of startup cash investment policy statement

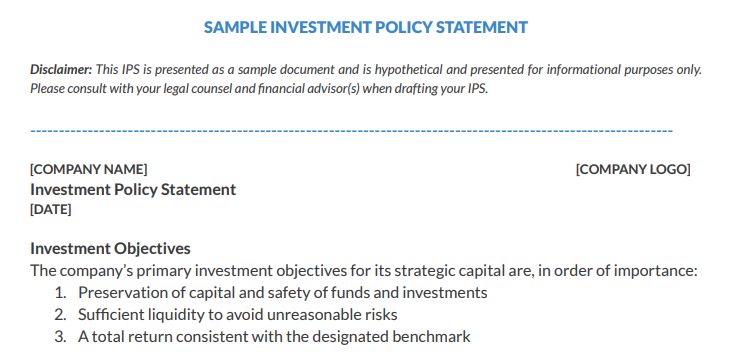

Investment objectives

Always remember that your primary goal for your startup’s cash reserves is safety. VCs and other investors will not be happy if you lose the funds they’ve entrusted to you to build your startup. Your second priority is liquidity. You need to make sure you can pay all your near-term expenses, even in the worst-case scenario. Don’t forget any outstanding one-time payments.

With those two goals firmly in mind, you can examine options that might provide you with a higher performance on your strategic funds, but startups should never chase yield at the expense of safety and liquidity. Again, you’ve got more flexibility with your strategic cash, but you definitely don’t want your money tied up in investments with long-term maturities that extend well beyond your runway.

Sample investment objectives guidelines

- Preservation of capital and safety of funds and investments

- Sufficient liquidity to avoid unreasonable risks

- A total return consistent with the designated benchmark

Roles and responsibilities

This section outlines the people who have authorization to carry out various responsibilities related to the investment plan. Those responsibilities include things like approving the IPS, authorizing any revisions, executing the investment policies, opening accounts, overseeing investments and their performance, and periodically reviewing the plan. Normally high-level management decisions rest with the CEO and board of directors. Employees with authority to manage the policy on a day-to-day basis include CFO, accounting management team, and any outside asset management firms you designate. NOTE: CEOs/founders should make sure that any transfer of funds must be authorized by them. Wire fraud is a serious issue, and founders need to take steps to guard against it – for most companies, this may be the part of their cash management plan most susceptible to fraud.

Best Practices On How To Prevent Wire Transfer Fraud:

- Always verify the authenticity and account information of each wire transfer request. This verification should be done by phone to a number on file or previously used, not one from the wire transfer request.

- Implement alerts through your online banking platform to notify you of any changes to payment instructions or other changes to any wire transfer process.

- Regularly review all wire transfers, account activity, and your bank statements for unusual transactions.

- Notify your bank immediately if you find suspicious activity.

Sample roles and responsibilities guidelines

IPS approval, IPS revision, opening investment accounts, transfer of funds (including wire transfers), and performance reviews

- CEO

- Board of Directors

IPS execution authority

- CFO

- Accounting management team

- Outside asset management team

Guidelines for investments

These guidelines list the types of investments that you consider appropriate for your startup and the currency you authorize (normally US dollars). Since safety is your primary objective, you will probably want to invest only in US Treasuries and money market instruments. Other options can include certificates of deposit (CDs), but if you cash those out early, you will lose any accrued interest, while Treasuries and money market funds will pay accrued interest. Some companies may choose to invest in commercial paper, which is an unsecured short-term debt instrument issued by large corporations with very strong credit. High-grade corporate bonds from very large corporations (think Google or Starbucks) are another lower-risk option (see below for more on investment ratings). Often, companies will also list prohibited investments, just to make it clear that some investment vehicles are off-limits.

This section also includes the minimum credit quality of the investments that can be purchased for the portfolio. Credit ratings from Nationally Recognized Statistical Rating Organizations (NRSROs), such as Moody’s, S&P Global, and Fitch, help control credit risk. Ratings are expressed as a letter grade and convey the creditworthiness of a government or business. US Treasury securities are not rated, since they are considered to be the most secure investments. However, money market mutual funds are rated by the NRSROs.

NRSROs can assign long-term investment-grade ratings (these ratings, from highest to lowest, are AAA,AA,A, BBB, BB, B, CCC, CC, C, and D). The agencies then use upper, mid, and lower ratings to give a finer degree of credit quality. Moody’s adds a number between 1 and 3, and S&P and Fitch add a + or a -. While the rating scales go to C and D levels, BBB is typically considered the bottom of investment-class securities. To maintain a Triple-A credit rating, money market funds have to meet stringent requirements and the ratings agencies review these funds regularly.

All three major NRSROs have also adopted a short-term rating system for securities that have maturities of less than 12 months. These ratings differ from the three-letter rating system.

S&P Global ratings use A-1 through A-3 (the highest classification), B, C, R (under regulatory supervision), SD and D (has defaulted on one or more financial obligations), and NR (not rated). Moody’s short-term ratings start at P-1 (Prime-1, the highest rating indicating a superior ability to repay debt), P-2 (strong ability to repay debt), P-3 (acceptable ability to repay debt), and NP (not prime). Fitch short-term ratings range from F1+ (exceptionally strong ability to repay debt), F1 (strong ability to repay), F2 (satisfactory ability to repay), F3 (adequate ability to repay), B (speculative), C (high possibility of default), and D (has failed on financial commitments).

Sample investment guidelines

Currency

- Funds will be invested only in instruments denominated and payable in US dollars.

Approved investments

- Obligations of the US government and its agencies

- Money market repurchase agreements

- Money market funds registered according to SEC Rule 2a-7 of the Investment Company Act of 1940

Prohibited investments

- Commercial paper (note: some startups will invest in this)

- High-grade corporate bonds (note: some startups will invest in these)

- Asset-backed securities

- Municipal obligations

- Collateralized debt or loan obligations

- Auction rate securities

Approved short-term credit quality ratings

- A-1, P-1, F1

Prohibited short-term credit quality ratings

- A-2. P-2, F2

- A-3. P-3. F3

- B, NP, B, and any lower ratings

Approved long-term credit quality ratings

- AAA/Aaa/AAA

Prohibited long-term credit ratings

- AA+/Aa1/AA+ and any lower ratings

Asset allocation requirements

Companies will specify what percentage of their overall portfolio can be invested in a specific security. Normally, diversification in an investment portfolio spreads risk around by investing in many different types of securities. For startups, however, the majority of their portfolios should be in short-term, very low-risk investments like securities issued by the US Treasury.

Sample asset allocation guideline

- 95% of the overall portfolio must be invested in US Treasury and US government agency securities.

Liquidity

Liquidity is a measure of how quickly and easily a security can be converted into cash relative to its market price. In other words, liquidity refers to how quickly and easily a financial asset or security can be converted into cash without losing significant value. Any investments in a startup portfolio should be easily sold priority to maturity if necessary to preserve capital or provide liquidity.

Sample liquidity guideline

- All securities held must be readily marketable with publicly available pricing and liquidity provided on a daily basis.

Maturity

Bond maturity is the time when a bond issuer must repay the original bond value to the bond holder. Startups typically should hold securities that mature in approximately one year or less, but there may be circumstances in which slightly longer maturities can be acceptable. Your burn rate, runway, and fundraising plans will factor into your decisions about the maturity of the securities you hold. Government money market funds are required to hold only securities that mature in 397 days (13 months) or less.

Sample maturity guideline

- At time of purchase, the maturity of each security in the portfolio will not exceed 397 days. The weighted average of any mutual funds held by the company will not exceed 397 days.

Performance

While performance is not the primary goal for startups, it’s useful to specify a benchmark against which the portfolio can be measured to make sure you’re getting a reasonable return. You should choose publicly available benchmarks that are clearly defined and that mirror your IPS strategy. Your benchmarks should match your asset classes or investment type. For example, if you’re invested in US Treasuries or government money market funds, the Lipper Institutional Money Market Fund Average provides average performance of all eligible institutional class money funds, or a 90-Day Treasury Index also may be a reasonable benchmark to use. If you choose to invest in commercial paper or high-grade corporate bonds, you should choose benchmarks that are appropriate for those securities.

This section may also spell out the frequency of meetings with outside investment management, any certifications investment managers must hold, and how often investment managers will deliver reports and statements. Any outside investment managers or firms should be a Registered Investment Advisor (RIA), which means they are registered with the Securities and Exchange Commission (SEC) or a state regulatory agency. RIAs have a fiduciary relationship with their clients, so they are required to put the best interests of their clients first.

Sample performance guidelines

- Any outside investment managers or firms will be Registered Investment Advisors (RIAs).

- The investment manager must verify compliance with the CFA Institute’s Global Investment Performance Standards (GIPS).

- The portfolio’s total return performance should be similar to the rate of return of the agreed-upon benchmark.

- The investment manager will meet with the company no less than four times annually and will be available for regular telephone contact.

- The investment manager will provide monthly statements of transactions and market valuation of portfolio assets.

Transparency

This section states what types of accounts can be used for the startup’s investments. It’s also a good idea to require a Statement on Standards for Attestation Engagements (SSAE) number 16 report, which is an auditing standard for service organizations established by the American Institute of Certified Public Accountants (AICPA) to help CPAs more accurately audit a company’s financial statements.

As noted earlier, you should always use a Registered Investment Advisor (RIA) to manage your portfolio. Your RIA should provide you with access to the right custodian for your assets. It’s very important that your assets remain in the name of your company, not in the name of a brokerage or bank. You don’t want your assets comingled with other funds and used as an asset on a company balance sheet. If your custodian runs into financial problems, you may not be able to get to your funds.

Sample transparency guideline

- Assets are to be held in a segregated third-party custodial account.

Your investment policy statement creates a framework for managing your assets, and it also puts up some guardrails to keep your assets from being mis-managed. Your IPS can also help bring new additions to your accounting/finance team or new board members up to speed quickly on your investment policies. Finally, an IPS also helps to reassure venture capital investors that you understand your fiduciary responsibilities and you’re prudently managing the capital they’ve entrusted to you. For more information about cash management and investment policy statements, please contact us.