Traditional businesses get loans, but startups sell pieces of the company. When you raise with SAFE notes or convertible notes, you’re effectively pre‑selling equity at a future discount or capped valuation. That doesn’t feel real until the first “priced round” (e.g., Series A), when those instruments convert into actual shares and your ownership share drops. The math behind caps and discounts determines how much you gave away in a Series A dilution. We’re going to run through some simplified examples to show you how this works, but first let’s summarize what we’re going to demonstrate:

- A discount SAFE just gives investors a percentage‑off coupon on the Series A price (for example, 20% off), which is usually milder on founder dilution than a low valuation cap.

- A valuation cap dilution can be much harsher. If the round prices at $20,000,000, but the cap is $10,000,000, the SAFE converts as if the company were only worth $10,000,000, driving a lower price per share, more investor shares, and more dilution.

- When a SAFE has both a cap and a discount, it always uses whichever yields the lower price per share, so the terms are “best of both worlds” for investors and most dilutive for founders when the round valuation is well above the cap.

- Lower‑priced rounds can flip the math so the discount, not the cap, drives conversion, which can still be more dilutive than a high cap because investors buy even cheaper shares.

- Stacking multiple SAFEs with different (especially lower) caps compounds dilution. A second, more aggressive cap can cost founders several extra percentage points of ownership without raising more total dollars.

- Across the scenarios, seemingly small differences in caps and discounts move founder ownership by 5-10+ percentage points by Series A, so founders need to model these terms in advance to clearly understand the startup cap table dilution, and walk into priced rounds knowing exactly where their ownership will land.

Capped Valuation and Discounts on SAFEs or Convertible Notes

Let’s define some terms, and then you’ll see how these concepts play into dilution as we go through the examples:

- A discount in SAFE notes or convertible notes says: “When the priced round happens, this investor gets to buy shares at a percentage cheaper than the new investors in that round.” It doesn’t cap the valuation; it simply applies a fixed percentage reduction to whatever price the round sets.

- A capped valuation is the maximum company valuation that will be used to calculate an investor’s price per share when their SAFE notes or convertible notes convert in a future priced round. In other words, even if your Series A is priced at $20,000,000, a $10,000,000 cap says, “for this investor’s conversion, pretend the company is only worth $10,000,000.” That cap drives a lower effective price per share and therefore more shares for the SAFE note/convertible note investor and more dilution for the founder.

Below, we walk through concrete, numbers‑driven scenarios that show how different terms – cap only vs. discount only vs. both – change founder ownership at the Series A.

Setup: Base Company Before the Series A

Assume:

- The founder owns 10,000,000 common shares (100% of the company pre‑financing).

- No option pool yet (we’ll keep examples focused on the instruments).

- The startup raises $1,000,000 via different SAFEs / notes before the Series A.

- The Series A is a $20,000,000 pre‑money valuation where new investors are paying cash for 25% of the company after all pre‑money securities (founder + SAFEs/notes) are counted.

To make the scenarios comparable, we’ll always:

- Convert the SAFE/note.

- Sell enough new shares so Series A investors end up at 25% ownership.

We’ll look at how founder ownership changes under three structures.

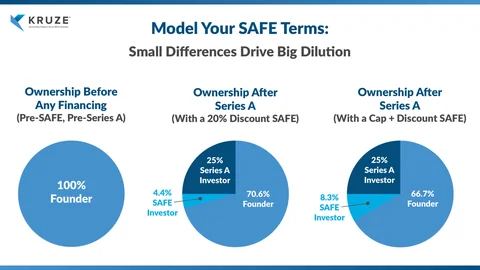

Scenario 1: SAFE with Only a 20% Discount (No Cap)

Terms:

- SAFE amount: $1,000,000

- Discount: 20%

- No valuation cap

Step 1 – Series A share price (undiscounted)

Assume the Series A price per share is set from the founder’s 10,000,000 shares:

Series A price = $20,000,000 pre-money / 10,000,000 shares = $2.00 per share

With a 20% discount, SAFE investors pay:

Discounted price = $2.00 × (1 - 0.20) = $1.60 per share

Step 2 – SAFE shares at discount

SAFE shares = $1,000,000 / $1.60 = 625,000 shares

Now the pre‑money shares before the Series A fundraise are:

- Founder: 10,000,000

- SAFE: 625,000

- Total pre‑money shares: 10,625,000

Step 3 – Issue Series A for 25% post‑money

Now we’ll need to do some more math. Remember, we want the Series A investors to own 25% of the total post-money shares. To find the number of shares the Series A investor we use this formula:

(Series A shares) / (10,625,000 + Series A shares) = 25%

Solving for the Series A shares gives us 3,541,667 shares that will be sold to Series A investors.

Now the post‑money share counts are:

- Founder: 10,000,000

- SAFE: 625,000

- Series A: 3,541,667

- Total: 14,166,667

And the post‑money ownership percentages are:

- Founder: 10,000,000 / 14,166,667 = 70.6%

- SAFE: 625,000 / 14,166,667 = 4.4%

- Series A: 25%

Bottom line: With a discount‑only SAFE, the SAFE investor gets shares at 1.60 vs. 2.00, and the founder ends up around 70.6% post‑money.

Scenario 2: SAFE with Only a $10M Valuation Cap (No Discount), Round at $20M

Now we’ll use a valuation cap instead of a discount.

Terms:

- SAFE amount: $1,000,000

- Valuation cap: $10,000,000

- No explicit discount

- Series A pre‑money valuation: $20,000,000

The SAFE converts at the lower of:

- The funding round price (based on $20,000,000).

- The cap price (based on $10,000,000).

The cap is better for the SAFE investor, since they get shares as if the company were valued at $10,000,000.

Step 1 – Cap‑based price per share

Using the founder’s 10,000,000 shares:

Cap price = $10,000,000 / 10,000,000 = $1.00 per share

(For simplicity, we’re assuming the same 10,000,000 shares are the capitalization base for both the $20 million pre‑money and the $10 million cap. In practice, you’d include options, etc., but the relationships still hold.)

Step 2 – SAFE shares at cap price

SAFE shares = $1,000,000 / $1.00 = 1,000,000 shares

Now the pre‑money shares before the Series A fundraise are:

- Founder: 10,000,000

- SAFE: 1,000,000

- Total: 11,000,000

Step 3 – Issue Series A for 25% post‑money

Again, we need to do some math. We want the Series A investors to end up with 25% ownership of the company. So our formula is:

(Series A shares) / (11,000,000 + Series A shares) = 25%

Solving for the Series A shares gives us 3,666,667 shares that will be sold to Series A investors.

Now the post‑money share counts are:

- Founder: 10,000,000

- SAFE: 1,000,000

- Series A: 3,666,667

- Total: 14,666,667

And the post‑money ownership percentages are:

- Founder: 10,000,000 / 14,666,667 = 68.2%

- SAFE: 1,000,000 / 14,666,667 = 6.8%

- Series A: 25.0%

Compare to Scenario 1:

- Discount‑only SAFE (20% discount): Founder owns ~70.6%

- $10M cap SAFE on a $20M round: Founder owns ~68.2%

That’s ~2.4 percentage points more dilution for the same $1 million of capital, just because the SAFE converts at a cap rather than a discount.

Scenario 3: SAFE with Both a $10M Cap and 20% Discount

Most modern SAFEs give investors both a cap and a discount, and they convert at whichever yields the lower price per share (i.e., more shares for the investor).

Terms:

- SAFE amount: $1,000,000

- Valuation cap: $10,000,000

- Discount: 20%

- Series A pre‑money: $20,000,000

From previous steps:

- Series A price: $2.00 per share.

- Discounted price: $1.60 per share (20% discount).

- Cap price: $1.00 per share ( from the $10 million cap).

The investor chooses the lowest price ($1.00), so this scenario is mathematically identical to Scenario 2:

- SAFE shares: 1,000,000

- Founder post‑money share of company: ~68.2%

- SAFE post‑money share of company: ~6.8%

- Series A: 25%

Bottom line: When the next round valuation significantly exceeds the cap, the cap dominates the discount and substantially increases SAFE dilution compared to a discount‑only structure.

Scenario 4: Lower-Priced Round Where Discount Beats the Cap

This time we’ll flip the situation so the next round is below the cap, making the discount the better deal for the investor.

Assume:

- SAFE: $1,000,000

- Valuation cap: $20,000,000

- Discount: 20%

- Series A pre‑money: $10,000,000

Step 1 – Round price per share

Round price = $10,000,000 / 10,000,000 = $1.00 per share

Cap price per share:

Cap price = $20,000,000 / 10,000,000 = $2.00

Discounted price:

Discount price = $1.00 × (1-0.20) = $0.80

The investor uses $0.80 (discount) rather than $2.00 (cap), because it’s lower.

SAFE shares = 1,000,0000 / 80 = 1,250,000 shares

Pre‑money shares before new cash:

- Founder: 10,000,000

- SAFE: 1,250,000

- Total: 11,250,000

Series A investors again buy 25% post‑money:

(Series A shares) / (11,250,000 + Series A shares) = 25%

Solving for the Series A shares gives us ~3,750,000 share

Now the post‑money totals are:

- Founder: 10,000,000

- SAFE: 1,250,000

- Series A: 3,750,000

- Total: 15,000,000

And the post‑money ownership is:

- Founder: 10,000,000 / 15,000,000 ≈ 66.7%

- SAFE: 1,250,000 / 15,000,000 ≈ 8.3%

- Series A: 25.0%

Here, the discount creates more dilution than a cap would have because the cap is above the actual round valuation. This shows why a combined “cap + discount” SAFE always gives investors the best of both worlds – and why founders must model both sides.

Scenario 5: Multiple SAFEs with Different Caps

Finally, consider how stacking SAFEs with different caps compounds dilution. For simplicity, assume:

- SAFE A: $500,000 at $10,000,000 cap

- SAFE B: $500,000 at $5,000,000 cap

- Series A pre‑money: $20,000,000

Using the same 10,000,000 founder shares as the base:

- SAFE A price: $10,000,000 / 10,000,000 = $1.00, which yields 500,000 shares

- SAFE B price: $5,000,000 / 10,000,000 = $0.50, which yields 1,000,000 shares

Pre‑money before Series A:

- Founder: 10,000,000

- SAFE A: 500,000

- SAFE B: 1,000,000

- Total: 11,500,000

Issue Series A for 25% post‑money:

The formula is (Series A shares) / (11,500,000+Series A shares) = 25%

Solving for the Series A shares gives us ~3,833,333 shares

So the post‑money totals are:

- Founder: 10,000,000

- SAFE A: 500,000

- SAFE B: 1,000,000

- Series A: 3,833,333

- Total: 15,333,333

The post‑money ownership is:

- Founder: 10,000,000 / 15,333,333 ≈ 65.2%

- SAFE A: 500,000 / 15,333,333 ≈ 3.3%

- SAFE B: 1,000,000 / 15,333,333 ≈ 6.5%

- Series A: 25.0%

Compare those totals to the single $1,000,000 SAFE at a $10,000,000 cap (~68.2% founder). Adding the second, more aggressive $5,000,000‑cap SAFE drops the founder another ~3 percentage points, without raising more total capital than $1,000,000. The terms changed, not the dollars.

Why This Matters for Founders

These simplified examples show a few key patterns:

- A cap that’s far below the next round valuation effectively pre‑prices a chunk of your company at a steep discount, often more dilutive than a simple percentage discount.

- Cap + discount SAFEs convert at whichever is harsher for you (lower price), which can significantly increase dilution relative to either mechanism alone.

- Stacking multiple SAFEs / notes with different caps and discounts magnifies dilution, especially when later ones have lower caps.

- By the time you reach a priced round, these early decisions can easily move founder ownership by 5-10+ percentage points, even if the total dollars raised were the same.

In other words: it’s not just about getting the money in the door. It’s about what those terms do to your cap table when the Series A dilution hits.

A startup-focused accounting and finance partner like Kruze Consulting can help you:

- Model valuation cap dilutions and discount‑driven dilutions before you sign anything.

- Build fully diluted cap tables that include all SAFE notes, convertible notes, and option pools.

- Walk into your priced round understanding where founder ownership will land under different scenarios, so you can negotiate terms with eyes wide open.