Venture Debt

Everything you wanted to know about venture debt

From a former Venture Debt partner - lists of the top funds, negotiating tips and term sheet guidance.

Kruze Consulting

Kruze Consulting’s Scott Orn was a partner at a major venture lender, and now provides consulting help to startups raising VC and debt. This page contains one of the largest and best lists of startup lenders - all of whom Scott knows well. If you’d like an introduction to a lender, click on those that interest you and he will get back to you.

You’ll also find podcast interviews with leading partners at banks and funds, plus the largest survey of the startup debt market ever conducted. There is also information on how to negotiate a startup loan, plus definitions of key terms that you’ll find in a venture debt term sheet. We have also released a sample venture debt term sheet that has helpful tips on negotiating with a lender.

Venture Debt Lenders

By clicking the card you can choose the lenders you want to contact.

Triplepoint

Summary

TriplePoint Capital is a Sand Hill Road-based global financing provider to high growth venture capital-backed companies throughout their lifespan, providing customized debt financing, leasing, and direct equity investments. TriplePoint provides unparalleled levels of creativity, flexibility and customer service to serve as the primary debt financing provider for leading venture capital-backed companies in the technology, cleantech and life sciences sectors and is the only debt provider equipped to meet the unique needs of high growth venture-backed companies at every stage of their development.

Western Tech Investment (WTI)

Summary

For more than 30 years, WTI has provided venture debt, a minimally dilutive form of growth capital, to high-growth public and private companies, including 3PAR, Ablation Frontiers, BeVocal, Brocade, Cerent, Facebook, Google, IDEC Pharmaceuticals, InvenSense, Juniper Networks, Neutral Tandem, Postini and Youku.com.

Bridge Bank

Summary

Bridge Bank was founded in the highly competitive climate of Silicon Valley in 2001, and continues to provide a full suite professional business banking services. From the very beginning, our goal has been to offer small-market and middle-market businesses from across many industries a better way to bank. A less bank-like way to bank. In June 2015, Bridge Bank merged with Western Alliance Bancorporation.

Arc

Summary

Arc is on a mission to help startups grow. We provide up to $50M in non-dilutive funding and a set of purpose-built financial tools to help startups save, spend and efficiently deploy their capital. Hundreds of startups have leveraged Arc to accelerate their growth, extend their runway and make strategic bets.

Brex, Inc.

Summary

Brex is a powerful financial stack designed to serve the next generation of growing businesses. By integrating software, services, and products into one experience, we help customers effortlessly extend the power of every dollar, so they’re free to focus on big dreams and fast growth—without worrying about wasted spend. Brex proudly serves tens of thousands of businesses, from small private companies to many of America’s most beloved public brands. Brex’s venture debt offering is designed for early-stage, venture-backed technology companies with a product-market fit, recurring revenue base, and scalable business model.

Hercules Capital

Summary

Hercules is the largest non-bank lender to venture capital-backed companies at all stages of development in a broadly diversified variety of technology, life sciences, and sustainable and renewable technology industries.

Horizon Technology Finance

Summary

Horizon Technology Finance Management LLC is a venture lender that offers growth-oriented loans to emerging technology, life science, healthcare information and services and cleantech companies. Horizon has provided over $1.3 billion in loan commitments.

Comerica

Summary

With more than two decades of experience, the Comerica Technology and Life Sciences Division has a thorough understanding of the specific banking needs of technology and life sciences companies. Comerica’s dedicated specialists also know the unique challenges entrepreneurs face and work one-on-one to create proactive banking solutions that fit individual needs. We’ve also developed relationships with top-tier investors who hold vested interests in funding start-up and emerging companies like yours.

Pacific Western Bank

Summary

At Pacific Western Bank, you will experience our unrivaled high-touch service, delivering quick turnarounds, transparent credit terms and thoughtfully structured banking solutions to preserve and manage your resources and capital. You will have an assigned client service team made up of senior bankers, making us nimble and highly responsive. We provide the best bespoke service, delivered with the speed and consistency that today’s innovators deserve.

California Bank of Commerce

Summary

The technology industry is unique, so your banking solutions should be just as specialized. Led by Bay Area and Silicon Valley professionals, the bank has dedicated expertise both in the banking and technology industries. From early-stage tech companies to the later stage publicly traded businesses, the experts at California Bank of Commerce are here to support your company through every stage of its growth. Our stage-based approach allows us to address your company’s needs and create a proven path for success. Our diverse debt and product solutions are customized to the distinct needs of your company – we offer robust, best-in-class services including treasury management and a commercial card, and we know tech! Our Technology Division is a team of Silicon Valley veterans who understand the industry and its ever-changing needs.

Avidbank

Summary

Avidbank's Venture Lending division provides a comprehensive suite of banking and financing solutions to technology sector entrepreneurs and their investors. With offices located in key innovation hubs nationwide, Avidbank is known for exceptional client service and innovative banking products, as well as collaborative debt solutions. Avidbank is experienced, accessible and responsive.

Top Corner Capital

Summary

Top Corner Capital is a new venture debt fund focused on early stage companies. It was founded by Patrick Lee who has 25 years of investing experience, including 10 years on the venture equity side and the last 15 years on the venture debt side. The fund will target tech companies in the enterprise, consumer and healthcare areas. Top Corner Capital will have the ability to focus and spend time with innovative entrepreneurs to help grow their businesses while complementing the existing equity firms and providing founder friendly capital with maximum flexibility and support. The Fund will also be making direct equity investments in select companies.

Braavo

Summary

Braavo is creating a better model for app companies to receive funding for growth — one that arms developers and founders with insights to scale sustainably and capital to turn their vision into reality. We’ve built a robust funding platform and a suite of powerful analytics tools that track and analyze app performance, enabling us to provide customized funding for companies of all sizes, stages, and categories.

Trinity Capital

Summary

Trinity Capital is a leading venture lender and valued partner to fast-growing companies across multiple stages and sectors. Since 2008, Trinity has worked closely with leading venture capital firms and their respective portfolio companies to offer valuable support, enhanced flexibility and competitive venture debt financing solutions to customers with distinctive needs. Trinity Capital is the partner of choice for venture-backed entrepreneurial companies wanting an experienced financial partner to strengthen their financial position while preserving equity.

Lighter Capital

Summary

Royalty Based financing vehicle that focuses on SaaS & Recurring Revenue businesses. Lighter Capital is venture capital backed

CSC Leasing

Summary

Startups often struggle with funding equipment acquisitions without disrupting cash flow and diluting ownership. CSC Leasing maintains a successful 35-year track record working with early stage organizations, providing a low-cost, non-dilutive form of capital for procuring equipment. Their leases compliment funding from venture and private equity sources, preserving investment capital for mission critical growth and other operating initiatives—not depreciating assets. Having financed over $1B in transactions and a wide array of equipment, CSC is experienced in crafting a tailored solution to match the capital requirements necessary to achieve business goals.

Signature Bank

Summary

Signature Bank (NASDAQ:SBNY) is a full-service commercial bank with almost $50 billion in assets. The Bank offers single-point-of-contact service that focuses on fulfilling the financial needs of privately owned businesses, their owners and senior managers. Signature Bank’s Venture Banking Group provides commercial lending and deposit solutions for venture-backed companies and their investors. The Group’s experienced team understands entrepreneurs’ unique challenges and needs and is committed to providing the expertise, flexibility and service to take your company to the next stage. Signature Bank is a Member FDIC.

Runway Growth Capital

Summary

Runway Growth Capital lends capital to late stage startups looking to fund growth with minimal dilution. We’ve built a diverse portfolio of high growth, asset light companies – both sponsored and non-sponsored – across a variety of industries. Our experience, patience and ability to navigate all market conditions make us a valued partner to entrepreneurs. We deliver creative, customized financing solutions that meet the needs of modern businesses.

Flow Capital

Summary

Flow Capital is an investor that provides minimally-dilutive growth capital for high-growth companies operating in the United States, Canada, and the United Kingdom. Our venture debt and revenue-based financing structures offer founders fast, flexible, and founder-friendly capital to grow their companies without giving up board seats or personal guarantees. While our primary focus is on the technology sector, we are open to high-growth companies operating in other non-tech sectors.

Espresso Capital

Summary

Espresso provides non-dilutive growth capital and bridge financing solutions to sponsored and non-sponsored leading North American companies in technology, healthcare, and other high-growth verticals. Since 2009, we’ve partnered with more than 260 companies and their investors to accelerate growth, extend the funding runway, reduce cost of capital, and minimize dilution.

Montage Capital

Summary

Montage Capital provides minimally dilutive growth debt to capital efficient companies with at least $3 million in annual revenue. Montage is uniquely positioned as a less dilutive alternative to equity financing, with the experience to offer guidance typical of equity investors. Montage is often the first institutional investor in a company, but Montage also supports venture or private equity-backed companies without requiring a concurrent equity investment.

Bigfoot Capital

Summary

Bigfoot Capital provides growth-oriented loans to SaaS businesses with $1.5M+ ARR.

Level Equity

Summary

Creative and flexible debt and debt/equity hybrid solutions to SaaS and technology companies with recurring revenues of at least $4M.

Data Sales Co.

Summary

Equipment Leasing Company

Coromandel Capital

Summary

Coromandel Capital's founding partners are veteran credit and technology professionals with expertise in structuring debt transactions. They bring specialization in working with founders to be thoughtful about non-dilutive growth capital.

Camber Road

Summary

Camber Road takes a different, debt-free approach to non-dilutive capital, providing leases—not loans—so there are no liens, restrictive covenants, personal guarantees, high interest rates or warrants. Camber Road’s model helps growing companies acquire equipment without using their equity dollars, financing stuff like manufacturing and warehouse equipment, custom devices, robotics, racking, laptops, tablets, and furniture - i.e. anything on a capex or FF&E line. The companies we work with find our structure creative, and our financing tends to extend their runway.

2019 Kruze Consulting Venture Debt Survey

Market trends and market size analysis

Firms that responded to this survey represent approximately 85% of the US venture debt market, and have close to $23 billion in outstanding venture debt loans - out of the approximately $26 billion in venture debt loans deployed in the past 4 years.

Venture debt is an important, but not well understood, part of the venture funded startup ecosystem, helping startups that have already raised venture capital access cheaper capital to boost their growth and achieve value creation milestones. We believe that this is the largest survey of the venture debt market. Kruze Consulting surveyed startup loan officers and partners at debt funds to understand the size and state of the market, to get information on trends in startup loan deal terms, and to learn about how venture capitalists and startup founders feel about this asset class. The respondents’ firms control well over half of the venture debt dollars in the United States, making this the broadest survey of this important, but not well understood, startup financing vehicle.

Why do startups raise venture debt?

According to the players surveyed in this report, the vast majority of startups that raise venture debt do so to increase their runway to make the startup more valuable at the next round.

This is consistent with the rest of the findings in the survey - the best use of this capital source is for startups that want an additional slug of capital to achieve their goals before raising another venture capital round.

What is the number one reason startups raise venture?

The US Venture Debt Market Size

The venture debt market is usually estimated to be roughly 5% to 10% of the venture capital market. In our survey, we asked how large the respondents thought that the market was for the past several years, and asked for a prediction on the market’s size for 2019. Given that our respondents’ funds control the majority of the market, we believe that their collective opinion is a strong indication of the market’s size and growth.

Venture Debt Market Size - $ in Billions

Our respondents predict a record-breaking year for the venture debt market, coming off huge growth in 2018.

We estimate that the US venture debt market was $8.4 billion in 2018, up from $6.5 billion in 2017 - almost 30% year over year growth.

For 2019, the venture debt market is predicted to be $10.1 billion, 20% growth off of 2018, and double what the market was in 2016.

This growth is driven by the hot VC fund raising market, with lenders making more capital available as startup raise more VC funding.

Comapring the Venture Capital Market Size to the Venture Debt Market

Venture Debt vs. Venture Capital Market Size

Comparing the VC market size (using data from PitchBook) to the startup loan market, we can see that the startup lending market follows the trend of the venture equity market, with both markets moving down in 2016 and up in 2017 and 2018.

With PitchBook and other VC industry data sources predicting 2019 to be a record-breaking year for venture capital, the prediction that the startup loan market will reach over $10 billion dollars makes sense.

“2019 is off to a strong start. Our clients are seeing more high quality deals than ever before, mainly driven by the robust venture capital market. I expect that 2019 will be the biggest year in the history of venture debt.”

- Scott Orn, Kruze Consulting COO

2019 Venture Debt Trends

Trends in deal terms also point to a hot market. Increasing deal sizes, decreasing interest rates and warrant coverage are all indicative of a competitive market, where players are fighting to get into the hottest companies.

Venture Debt Deal Sizes

Are venture debt deals getting smaller, staying the same or getting bigger in 2019?

Over 70% of our respondents believe that venture debt deal sizes are getting bigger - and none responded that they are shirking in 2019.

Most lenders use a rule of thumb of 20% to 40% debt to equity when committing to a deal. Therefore, as equity rounds get bigger, it’s only natural for the debt deals to get bigger too. Also, lenders are like every other asset manager, bigger deals are better for profits, management fees and carry. Another factor creating larger deals is that the banks in the sector have never been more liquid because they are sitting on the deposits coming in from those huge equity rounds. The final way the hot equity market drives more leverage is that the reward for a startup to hitting their milestones has never been greater in the form of a big up round valuation. A loan gives startups that extra runway insurance that gets them over the hump and makes that big round possible. Why risk falling a few months short of a big milestone when taking debt can get you there?

Interest Rates

How do interest rates compare this year to 2018?

Kruze’s venture debt survey is predicting over a 50% chance that rates stay the same or are lower in 2019, which is good for the startup ecosystem.

Stable interest rates are beneficial to startup borrowers because eventually venture loans need to be paid back. Almost every VD loan has a clause that allows the interest rate to float up if rates move up. Rising rates makes it harder for startups to pay back the debt and increase the cost of borrowing. Higher rates also reduce the advantage of taking a little bit of debt over more equity. If the debt gets too expensive, then founders aren’t really saving much with debt and should just take more equity.

Lower interest rates also keep the lenders flush with capital. When Interest Rates are low in the general market (US Treasuries & Foreign Bonds), then capital looks for higher returns in riskier sectors like venture debt. Capital flight to riskier asset classes is one of the reasons the lenders have so much capital at their disposal right now. If rates go up in the broader economy, then some of the capital will flow back into less risky bonds assets and leave venture debt.

Interest Only Periods

We asked if participants are seeing interest only periods shortening, staying the same or growing in 2019 vs 2018.

Interest only periods are the number of months a startup can use the capital without having to pay back any principal.

Eventually venture loans amortize (i.e. the borrower starts to pay back the loan) but the longer a startup can use the capital, the more progress it can make and better it’s next equity round.

When lenders are risk averse, they shorten the interest only period to get paid back faster, thereby de-risking the loan. Everyone of our survey respondents said Interest Only Periods are getting longer or staying the same, not one said they are getting shorter.

This is an extreme sign that the venture debt market is hot.

Are Lines Getting Used

Are lines getting used? We asked if the lines are not being used, getting partially used or being fully drawn.

In most instances, startups contract with a venture debt provider for the right to access a loan if they should want it. This is called “drawing down” the line or loan.

When capital is scarce, like in a downturn, most venture debt lines are fully drawn down.

However, in hot equity markets often the next round is preempted by an outside VC firm that “just wants in” and is less sensitive to price.

In our survey, we’re seeing over 70% of the survey participants saying more loans are not being used or getting fully drawn down, which is another extreme sign that the startup market is very hot. Startups have the luxury of not needing the debt capital because equity is so plentiful.

Warrant Coverage

Is warrant coverage down, the same or up vs. 2019?

Warrant Coverage is another method that lenders generate a financial return (in addition to interest). Getting Warrants, or Equity, in the startups gives the lenders huge upside and helps them offset some of the credit losses when startups go under.

When competition is tough for deals, lenders reduce the warrant coverage on the deals - aka reduce the price of the loan - to win the deal. When capital is scarcer, lenders can move warrant coverage up and get a bigger piece of the startup equity.

Less than 10% of the survey respondents are seeing warrant coverage going up, which means the sector is hot and very competitive.

Venture Capitalists and Startups Founder’s Knowledge of Venture Debt

Venture debt is more complicated than venture capital, and is less well understood by players in the startup ecosystem. That’s part of the reason Kruze offers venture debt consulting - we help our clients make the best use of this for of financing. In this survey, we asked our experts questions about how well startup founders and venture capitalists understood the market.

How Educated are Startup Founders and VCs on Venture Debt

Venture debt professionals were asked to rate startup entrepreneurs and venture capitalists education levels on venture debt.

Out of a 10 point scale, with 10 being very educated and 1 being not at all educated, our respondents gave startup entrepreneurs a 4.7 and VCs 6.7.

This suggests that startup founders are not very knowledgeable on venture debt. Anecdotally, this makes sense, as entrepreneurs tend to love venture debt because they don’t have to sell as much of their company’s equity. Because VC’s have pro rata rights, pretty much all dilution comes from founders so it’s natural that they are dilution sensitive.

Entrepreneurs believe in their mission so they don’t dwell on downside scenarios where the company goes bankrupt or the next round of funding is difficult and it becomes hard to pay the loan back. By definition, they have to believe they will hit their plan and raise a big up round. Contrast that with VC’s who have a broad portfolio of startups and see the traditional mix of 20% successful and 80% failure. Therefore, VC’s tend to understand the downside much better than entrepreneurs.

Some of the key misconceptions that our survey respondents had about entrepreneur’s misconceptions of this asset class were:

“Most startup entrepreneurs are not sure about the use of venture debt and the best time to take on venture debt is when you actually don’t need it. Debt providers view the debt as less risky when companies have sufficient cash levels when raising the debt.” Often times companies wait until they are very tight on liquidity and the debt analysis becomes harder. It is easier to raise - and draw down an existing line - when a company is doing well (or has a lot of cash on the balance sheet). Lenders are not in the business of helping failing startups extend their runway, so trying to raise this kind of capital when the company does not have a lot of runway is a mistake. And since most agreements have covenants about the startup is allowed to draw down/access capital from the lender, an entrepreneur will find it harder to get capital from their lender if they wait until the company is close to running out of cash.

“Don’t realize that a MAC or Investor Abandonment gives the lender a lot of control.” These two terms allow a lender to put the startup into foreclosure and take control of the business - never a good thing for the founders and investors. When a lender invokes a MAC (Material Adverse Change) clause, the lender is claiming that something has changed and the borrower will likely not be able to repay the loan. Investor Abandonment means that the lender has asked the existing venture investors to show their continued support of the business, usually by putting more cash into the company, and the VCs have declined.

“The largest debt offer or cheapest debt offer is not always better.” Several of the respondents mentioned some version of this common entrepreneur misconception. In the venture debt market, providers strive to differentiate beyond the size of the check or the interest rate/warrant coverage. Besides the “adding value” to their portfolio companies, different players have different clauses to their loans that can add or decrease the cost of the loan to the startup.

Do startup players think favorably of venture debt?

We asked, on a 10 point scale, with 0 being not at all favorable and 10 being very favorable, what founders and VCs thought of this financing vehicle.

Our findings that Startup Founders tend to like venture debt more than VC’s is consistent with anecdotal evidence in the market.

A big part of this is that Entrepreneurs really dislike dilution while VC’s can always do their pro rata to protect against dilution. So entrepreneurs love any capital that is less dilutive - like loans.

VC’s are more skeptical of venture debt because they have a large portfolio and they can see across the portfolio that sometimes companies don’t make it.

In those situations, Lenders & VC’s have to work through a shutdown or acquisition.

Having a lender in the mix makes downside scenarios more complicated and difficult for everyone - VC’s liquidation preferences are subordinate to the venture loan getting paid back so they are less likely to get their capital back in a downside scenario.

An Overview of Brex Venture Debt

In August 2021, Brex announced a $150 million venture debt fund. Everyone thinks of Brex as a credit card, but they also have Brex Cash, which is basically a “bank lite” feature. And offering a Brex venture debt fund is basically an extension of what the other startup banks do.

We don’t yet know if Brex is doing a fund or if they are lending off of their balance sheet or if they are lending out of their client deposits. But what we do know is that they currently are offering very competitive terms vs the incumbents. You can read all of our thoughts on Brex Venture Debt here.

Conclusion

The 2019 venture debt market is hot, riding off of a strong 2018 and record-breaking venture capital investments. We expect 2019 to be the largest year for venture debt, with lenders aggressively competing for the best startups - offering larger deals, more favorable terms and moving fast.

Startup founders should take advantage of this hot market to augment their cash balance with less dilutive debt.

However, founders need to remember that debt funds and banks like to invest when a company has recently raised VC or has a strong balance sheet.

They should also pay attention to the specific terms that they are offered during a raise, making sure that the lender’s interests are aligned with their own.

Kruze Consulting’s Scott Orn, a former partner at a major venture debt fund, offers venture debt consulting to help startups make the most out of a fund raise. If you are a venture funded startup, reach out to Kruze to learn more!A quick note - for early-stage companies looking for information on the CARES Act PPP loans, we have information on our CARES Act page.

Simplify Your Startup’s Venture Debt Process

Venture Debt Fetch connects startups to the best banks and lending funds, then analyzes the 1st term sheet for free!*

Venture Debt Podcasts by Kruze

Venture Debt Posts by Kruze

KRUZE CONSULTING BLOG

Some of our latest blog posts on venture debt. Visit all of our blog posts on startup debt .

Venture Debt Deposits Cover Legal & Documentation Costs

Venture debt deposits are typically required when a startup founder signs a venture debt term sheet for a couple of reasons. Your lender wants you to have some “skin in the game,” demonstrating that you’ve got a level of commitment to closing the deal and won’t just stop returning calls or emails. In addition, venture debt deals require due diligence, administrative costs, and documentation fees. Like any lender, they want the startup that’s asking for a loan to pay for those expenses.

Can Venture Debt Block You From Raising Equity?

Venture debt overhangs refer to startups that have taken on so much venture debt, it’s affecting their ability to fundraise. Venture capitalists don’t want their funds used to service a large debt load – that’s not a good investment for them. So that slows or even halts additional funding rounds. Startups need to be very careful about how much venture debt they take on.

How to negotiate a deal

The first step to negotiate a deal with a lender is to have multiple term sheets to compare

You Make The Decision

We’ll help you compare existing and new offers from a variety of lenders. You’ll have the freedom and advice to make the best decision for your startup. No information is shared without your consent.

Venture Debt Industry Expertise

Venture Debt Fetch allows you to compare all aspects of your term sheets. Get insights based on our years of debt & lending experience. Choose the perfect venture debt offer that aligns with the needs of your startup.

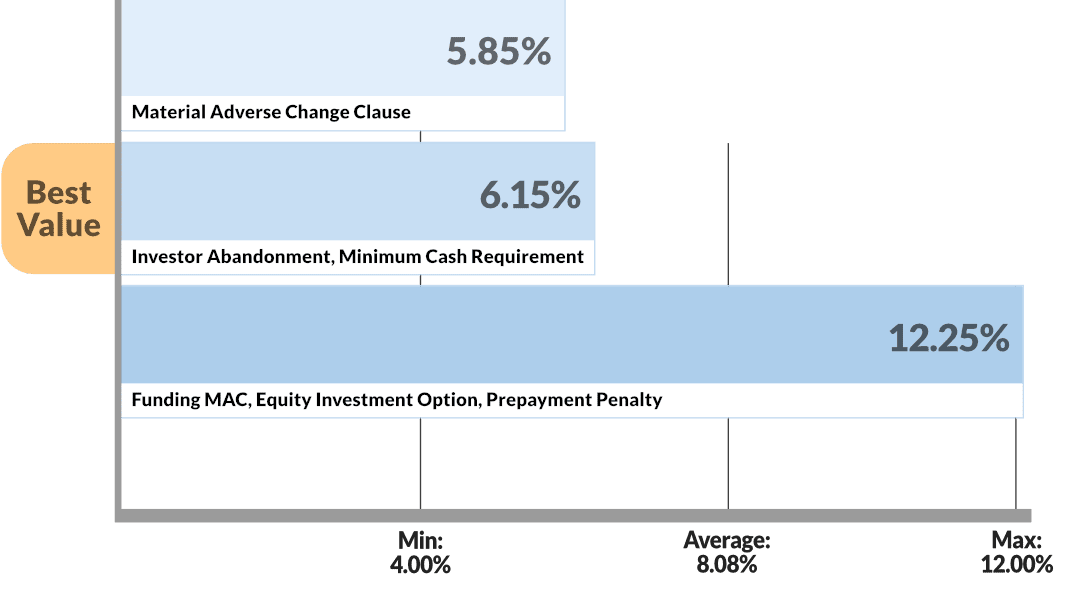

| Lenders | Lender A | Lender B | Lender C |

|---|---|---|---|

| Rate | 5.85% | 6.15% | 12.25% |

| Investor Abandonment Clause | ✔ | ✔ | |

| Funding MAC | ✔ | ✔ | ✔ |

| Minimum Cash Requirement | ✔ | ||

| MAC as Event of Default | ✔ | ||

| Prepayment Penalty | ✔ | ✔ | |

| Equity Investment Option | ✔ |

Analyze Your Term 1st sheet

Using state of the art technology and industry expertise, we will analyze your first term sheet for free.* We can help you through every step of the process: from understanding key terms to getting the best deal.

Venture debt playlist

Watch all Venture Debt Videos from Kruze Consulting

Key Terms

- 4 Reasons to Raise Venture Debt

- 5 Things to do after You Raise Venture Capital

- Acconts Receivable - Term of Loan

- Accounts Receivable Line

- Additional Indebtedness

- Advance Rate on Receivables

- Average Venture Debt Interest Rates

- Average Warrant Coverage on Venture Debt Deal

- Bank Letter of Credit

- Commitment Amount

- Dangers of Venture Debt

- Draw Period

- Eligible Receivables or Borrowing Base

- Equity Investment Option

- Final Payment

- Fintech Equity & Debt Staircase

- Fund Venture Lenders Vs. Bank Venture Lenders

- Funding MAC

- Growth Capital - Term of Loan

- Growth Capital Line

- How Kruze Consulting Helps Startups Get Venture Debt

- How to get an extension on a venture debt line

- Interest Only Period

- Investor Abandonment Clause

- Lien on Intellectual Property

- Material Adverse Change Clause (MAC)

- Minimum Cash Requirement in Venture Debt Deals

- Paid Time Off (PTO) Triggering Insolvency

- Prepayment Penalty

- Refundable Commitment Fee

- Springing Lien in a Venture Debt Term Sheet

- StandStill or Cooling off Period in Venture Debt

- Typical Interest Rate on Accounts Receivable Line

- Typical Interest Rate on Growth Capital Line

- Typical Warrant Coverage on an Accounts Receivable Line

- Typical Warrant Coverage on a Growth Capital Line

- VC Liquidation Preferences

- Venture Debt and the CARES Act

- Venture Lender's Startup Due Diligence Checklist

- Venture Lending Common Events of Default

- Warrant Coverage

- Warrant Coverage Upfront or On Usage

- What Are Prevailing Interest Rate and Warrant Coverage for Venture Debt

- What is a right of offset

- What is Venture Debt?

- What to do if you can’t raise Venture Debt?

- Why Do Startups Take Venture Debt?

- WTI Prepayment Penalty

- Top 6 mistakes companies make when raising venture debt

- What Do You Need To Know About Venture Debt Drawdown Period?

- Venture debt for startups: Don’t borrow your own money

- Is a flat interest rate or deferred interest better for startup venture debt?

- What is a negative pledge on IP?

- Sample venture debt term sheet

- Negotiating How Much Cash To Keep In The Bank

4 Reasons to Raise Venture Debt

Startups raise venture debt to extend their runway and by enough time to hit milestones, it must unlock to raise its additional capital. Runway extension is the most important reason for Venture Debt.

Another reason to raise venture debt is to refinance existing debt. When a startup completes an equity round, it’s time to shop the deal and refinance with either existing lenders or bring a new lender into the company. Refinancing debt also extends a startup’s runway.

A third reason is to fund an opportunistic new project that isn’t in the startups budget currently but will add tremendous value. A little extra cash from the debt can fund an optional but value-add project.

The fourth reason is to create optionality if the company is in acquisition talks with an acquirer. Venture debt doesn’t require resetting the company’s valuation in the way a new equity round would reset the valuation. Once the valuation is reset higher, the acquisition price must be higher and the new investor must agree to the deal.

5 Things to do after You Raise Venture Capital

First, you’re going to need a bank to deposit that big VC check. :)

It’s best to work with a bank that focuses on startups. Kruze Consulting loves First Republic. These banks specialize in startups. Their customer service is fantastic and their online banking systems are great which makes it easier for us and lowers your bill. If you need a referral to First Republic, just let us know!

Second, it’s a good time to start expanding your recruiting work. Entrepreneurs often underestimate the ramp time to actually hiring new team members, and if you fall behind in recruiting, you’ll fall behind on your operating plan and milestones. We recommend “Recruit” to jump-start your recruiting efforts. Don’t delay your recruiting, you’ll fall behind.

Next, you need an accounting firm! Kruze is the best and we’ll handle your taxes, your monthly accounting, give you a Fixed Fee for your Monthly Close. Having accurate financials allows you to pinpoint where you’re spending your money and report back to your VC’s. VC’s need real reporting and also want the company to be in Compliance (Taxes, State Registrations, etc). Hiring an accounting firm like Kruze will solve this problem and give you peace of mind too.

Fourth, it’s never too early to plan for your first board meeting. That first meeting is the foundation of the relationship of the relationship with your VC’s. If you’re prepared, have accurate financials and lay out your milestones, your VC’s will breathe a sigh of relief. Discuss your key initiatives, where you’ll be spending the VC’s money and drive a consensus. If the first Board Meeting is done right, it will instill a lot of confidence in your VC’s.

Finally, you want to start evaluating Venture Debt. Lenders love to come into a company that has raised a fresh round of equity. That way there is no adverse selection for them. Everyone is happy and it’s easier for the lender to make a commitment. The old saying, “You need money to borrow money,” is true. Lenders will give your startup a forward commitment so you can draw the money in the future when you need it and that way you don’t have to draw the money right away and needlessly pay interest. Get the debt in place right after the round and you’ll be happy you have that runway extension later. So, to reiterate, establish a startup bank (First Republic), accelerate your recruiting efforts, hire an Accounting firm like Kruze Consulting, prep for your first board meeting and put a venture debt line in place!

Acconts Receivable - Term of Loan

A/R Loans are typically 18 month commitments. They range from 12 to 24 months. At the end of the loan period, a bank will need to renew the Accounts Receivable Line. A startup should start planning 6 months in advance for renewal.

Accounts Receivable Line

An Accounts Receivable Line is a type of debt financing based on an advance of the eligible accounts receivables outstanding. Inexpensive debt because Accounts Receivable is really strong collateral. Banks typically control the startups cash too which is a second form of collateral.

Additional Indebtedness

Lenders want to control the total amount of debt a company carries because 1) the lenders don’t want to over-leverage the company and 2) if the lender is not secured in all the assets including Intellectual Property, then the lender must split the proceeds of the sale of assets where a full lien is not secured with the other unsecured lenders. Therefore, Lenders will often dictate how much other debt a startup can take on and often insist it is subordinate debt.

Advance Rate on Receivables

The Advance Rate on Receivables is the percent of eligible receivables a bank will give a startup. Most banks will advance 75% to 80% of an eligible received balance. This creates some margin for error for the lender should the company struggle and a portion of the Accounts Receivable proves uncollectable.

Average Venture Debt Interest Rates

There are two types of venture debt deals.

There’s a bank term sheet and then there’s the fund term sheet. The banks, again, are usually a little bit more restrictive and use investor abandonment clauses so they can be more aggressive on the interest rate; aggressive being lower. A typical bank interest rate will be somewhere around five, five and a half, six percent all in. That’s the cash interest you’re paying every year on the money you borrow.

Now, funds, they actually let you use the money a little bit more fluidly and so they don’t have the MAC or investor abandonment. Therefore, they need to charge more. Thus, the average interest rates we’re seeing on fund term sheets are somewhere around ten and a half to twelve percent. That’s the TriplePoint, WTI, type of deals. All in ten and a half to twelve percent interest rates.

Sometimes the upfront interest rate is a little bit low like maybe 8 percent. And then there’s a final payment that is paid at the end of the loan which brings the total IRR up to that ten and a half percent range.

Average Warrant Coverage on Venture Debt Deal

A typical venture debt deal can be kind of two flavors.

First is the bank, and again banks use investor abandonment, some of the stricter clauses, so they can be more aggressive on warrant coverage. And by aggressive, I mean ask for less work and less ownership in your startup. A typical bank warrant coverage will be somewhere around 1 percent of the deal amount so, to a million-dollar loan, 1 percent of that would be ten thousand dollars in a warrant, something around there.

Now, usually, you can also translate this to fully diluted ownership in the startup and that’s usually going to be around .1 percent. So, point .15 percent of the startup. So, again, banks are cheaper because they use more restrictive clauses. Nothing wrong with that. They’re upfront about it. Just know that’s going in.

The second type of lender is a fund lender. Now they’re letting you use the money a little bit more flexible and in a more flexible manner. And so, they’re going to charge more. They don’t have the MAC. They don’t have the investor abandonment. Typical warrant coverage for fund lender is anywhere from 6 to 10 percent of the deal.

So, again, in that million-dollar deal scenario, we’re talking from 60,000 dollars to 100,000 dollars of warrant coverage or equity in your company. Now, that usually translates to about 25 to 50 basis points of the entire company. Sometimes, when the fund lender is being very aggressive and giving you a lot of money, that number can actually edge up to 1 percent of the company total value or total ownership.

Now again, the great thing about venture debt is it’s less dilutive. So, you’re getting a lot more cash and you’re giving up less ownership. However, you always need to remember that this money needs to be paid back. Investor equity dollars don’t necessarily need to be paid back. Or in a downside scenario aren’t going to be paid back. So, the lender is trading off a lot of risk for a lower return.

And so, again, we see on average warrant coverage for a bank is going to be somewhere around 1 percent. And for a fund lender that’s going to be six to 10 percent of the deal amount and for the bank that’s going to translate to about .1 percent of the company.

And for the fund lender, it’s going to be a point to .25 percent to .5 percent. Those are averages but that’s typically what we see at Kruze Consulting when we’re negotiating venture debt deals.

Bank Letter of Credit

The big reason why startups use letters of credit is to give their landlord at their new office space a defacto deposit. It’s basically collateral for the landlord. And so, what the startup will do will have their bank issue a letter of credit may be for $100,000 maybe for $200,000. The bank will segregate that cash out of the startup’s normal operating account, back the letter of credit with that cash, the startup can’t touch it anymore because it’s backing that letter of credit, and then the bank hands over the letter of credit to the landlord.

Now, this is preferred because you’re not… You don’t necessarily want to transfer a hundred, two hundred thousand dollars to your landlord. and just hope they’ll get it back for you. Having the bank on your side, having it documented in a letter of credit is much safer for the startup, and it’s much easier logistically.

So that’s why startups use a letter of credits. There’re a few other reasons like inventory deposits or things like that, but it’s almost always used to secure new office space.

Commitment Amount

The total amount the lender is willing to lend. However, often the total loan amount is spread over time with separate tranches that can be unlocked by business milestones.

Dangers of Venture Debt

Debt can be highly effective for a startup to extend its runway and then hit a big milestone that makes fundraising easy and leads to an up round. However, if a startup over-leverages itself and raises too much debt, the company can become impaired and future fundraising gets really difficult. Don’t raise too much debt and put your startup at risk! We recommend raising no more than six months of extra runway. The biggest reason debt can hurt your startup is that the next investors will not want to see their new capital go to pay back the lender. They’re investing to help grow the company, not to de-risk and pay back the previous lender. Too much debt can create an overhang for new investors. Our simple guidance is to raise three to six months of runway. Startups often unknowingly sign up for dangerous terms like MAC (Material Adverse Change) or Investor Abandonment Clause which can create a default at the worst times. Those terms give the lender a lot of leverage over the startup if things go wrong. To summarize, don’t over-leverage your startup and raise more than 6 months of runway in debt, and beware MAC’s and investor abandonment clauses.

Draw Period

A venture loan is typically available for a fixed amount of time. The draw period outlines the dates by which the borrower must pull down the loan. Often a specific amount of debt must be drawn before an initial draw period ends. If the initial draw is completed, then the remaining loan balance might have an extended draw period into the future.

Eligible Receivables or Borrowing Base

A venture lender does not like old receivables, customer concentration or foreign receivables. Therefore the lender will generally limit the amount one customer or a group of customers, like foreign customers, can make up of the overall receivable balance for the startup that they are lending to. Customer concentration limits are usually around 20% - 30% of a receivable base. After subtracting out old receivables, customer concentration and foreign receivables, the startup is left with a $ amount, or borrowing base, that the lender will advance a percent against.

Equity Investment Option

Lenders build large portfolios of startups, and like all investors, want to get more ownership in the very best startups. Therefore they will often ask for the option to invest a specific amount of equity in future rounds. Letting the venture debt firm have too much of your next equity financing round can cause problems if the round is over-subscribed, so be careful with this term.

Final Payment

Successful startups typically raise future venture capital rounds at higher and higher valuations, meaning future capital is less dilutive, or “cheaper” than current capital. Therefore, venture debt providers will often ask for a payment at maturity that boosts the overall IRR of the loan but will be 3 or 4 years out into the future. This effectively backloads interest when it is less expensive for the startup. The lender hits its return hurdle and the startup back loads interest when the capital to pay it back comes from a less dilutive source.

Fintech Equity & Debt Staircase

Fintech companies have special capital structure considerations, especially when it comes to mixing debt and equity to drive growth. Fintech startups should start by raising equity capital to prove out their business model. As they are working on getting the business model doing, by burning that equity cash, they will want to find a debt partner who will help them in the next stages of their growth. At the Series A, they should consider raising a combination of equity and non-equity capital to fund the business. Listen to our video to learn more.

Fund Venture Lenders Vs. Bank Venture Lenders

Banks are able to lend to startups cheaply because their source of funds (customer deposits) are inexpensive because interest rates on checking and savings accounts are almost zero. However, Banks are Federally regulated and must be careful not to lose customer deposits on bad loans. Therefore, they rely on Material Adverse Change Clauses (MAC), Investor Abandonment Clauses and Other Covenants to control their risk and limit their losses.

Most banks have moved away from MAC clauses, but almost all bank term sheets include investor abandonment clauses. This term means a bank can force your investors to put more money in the company and if investors don’t act, then it becomes an event of default. Once a company is in default, the bank can sweep the cash to make themselves whole. Banks do this rarely and don’t like doing this, but it is the way they manage risk and losses.

In summary, banks leverage their low cost of capital from customer deposits, and the ability to use an investor abandonment clause, to lend cheaply. However, remember banks are not very flexible and need those covenants in the deal.

Comparing the Banks vs. Fund Venture Lenders, like a BDC or actually a pure venture capital fund, you’ll see Fund lenders are much more flexible but more expensive. Fund Lenders cost of capital is much higher because they are getting money from big institutions like endowments, foundations, and/or public investors (BDC) so they have to deliver a high return for those investors.

Fund Lenders justify the higher cost is by providing a high degree of flexibility. No material adverse change clauses, no investor abandonment clauses, providing larger deal amounts than banks would provide a startup, and longer interest-only periods.

So, Kruze Consulting views Funds and BDCs as flexible, very aggressive, but expensive. Banks are very conservative, like to tie you up a little bit, but are very cheap.

Startup Founders have to decide what type of lender and what type of risk profile they can live with. Founders spend many years of their life building their companies. Lenders can alter the mix between the VC Investors and Founders, At Kruze Consulting, we have many clients that borrow from banks because of the Founders and Board like the cheap cost of capital. At the same time, many startup clients will borrow from fund lenders because they’re willing to pay for that extra flexibility, extra dollar amounts, and extra interest-only periods.

Kruze has done the work for you by compiling summary scouting reports on the premier startup banks: Square 1 Bank, Comerica, City National Bank, and Bridge Bank.

Kruze has also developed scouting reports on these funds: Western Technology Investments (WTI) and TriplePoint.

Funding MAC

This venture debt term allows the lender to refuse new loan drawdowns if there has been a Material Adverse Change in the business. This clause gives the lender wide latitude to refuse a drawdown. It’s less dangerous than a MAC Default that can put the startup into foreclosure, but it can be used to deny the startup funding. It’s an important term if the startup is planning on drawing the capital far into the future. It’s less problematic if the startup will draw the capital immediately, since you’ll already have the funding from the loan in the bank and won’t have to take future drawdowns.

Growth Capital - Term of Loan

Venture Loans typically run from 30 to 42 months. A typical structure is interest only for 6 to 12 months and then monthly principal and interest payments ranging from 24 months to 36 months.

Growth Capital Line

A flexible but expensive loan product. A Growth Capital Line is not tied to specific collateral like a Accounts Receivable, but instead collateral will be all of the startups assets. Including Intellectual property into the collateral is negotiable. Often a negative pledge on IP is negotiated meaning the startup cannot pledge the IP as collateral to another lender, but the growth capital lender does not have a lien in the IP. The lack of IP lien can dramatically slow the foreclosure process, so the startup should avoid pledging the IP whenever possible.

How Kruze Consulting Helps Startups Get Venture Debt

The first step in Kruze Consulting’s Venture Debt process is to sit down with the CEO and determine if the debt is a good fit for the company. When the business is on the downturn, debt is not a good idea because adding a senior secured creditor to the mix only makes life more difficult over the long term. The next fundraise can be messy if a majority of the proceeds will go to paying back the debt. However, if the business is booming and you’ve recently completed a round, venture debt with a forward commitment to draw down is a great tool to put in place.

Especially after raising a new VC equity round, the company is in great shape and there is little risk of asymmetric information for the lender. That’s when a debt vehicle should be put into place.

After determining whether the debt is a good fit, Kruze will make introductions to its preferred lenders. Our team knows all the lenders so it’s easy to kick the process off quickly.

There is a temptation to talk to tons of lenders but we recommend a bank and two fund lenders to start. Once you get traction, you can do a couple more meetings to help optimize terms. More than three lenders can be a distraction. After introductions, Kruze will assemble a powerpoint pitch deck, historical financial statements, future projections, a cap table, and 409A valuations. These are the core pieces of information that lenders want to review.

After the lender reviews the materials, the deal sponsor will engage their credit committees and decide on a term sheet. As soon as the term sheet reaches the startup, Kruze will analyze the offer, explain all the difficult debt terms, explain to the CEO and Board of Directors what the term sheet means for the startup, model out the incremental runway from the debt and overlay the runway with the key milestones for the next fundraise. Kruze will model out the IRR, or cash cost, of the debt so Management knows how expensive the debt actually is for the startup. We’ll also model out and explain the warrant coverage, or equity upside, so Management and the Board know how much of the company it is giving away. Venture Debt is all about extending runway so a startup & CEO should be sure they’re buying enough insurance to achieve their milestones and raise an up valuation round.

Kruze will also walk Management through downside scenarios – if the startup is not achieving its milestones, how badly will the debt hurt the company?

After negotiating the debt deal and reaching a signed term sheet, Kruze will assist in the documentation process although this is mostly the domain of company counsel. Usually, a term or two become critical during negotiation and Kruze can assist the lawyers to explain the pros and cons of Management. Startups usually engage a venture debt specialist at their favorite law firm and those lawyers do a great job. It’s best to use experienced venture debt lawyers who can advise how key terms can affect the company’s business. Once the deal is documented, Kruze will advise on when the capital should be drawn down from the lender. That’s the venture debt process from start to finish and how Kruze Consulting can help!

How to get an extension on a venture debt line

Asking for an extension on a venture debt line is a pretty common request from startups. They do this because they want to be able to preserve the ability to draw the loan, but don’t need it quite yet. So they’re going to ask the lender to extend that drawdown period.

If it’s a short drawdown, the lenders are usually pretty happy to comply. After all, they want you to draw the money down. That’s how they make money on interest.

However, it’s going to be a lot easier if it’s a short term extension, like one or two months, because anything longer than that, they’re starting to extend the risk.

Tips for maximizing the chances of getting an extension: Have this conversation at least two months before the extension, before the original line runs out. Don’t do it last minute, in the last couple of weeks before your drawdown period ends. Provide an update on the company how business is going, your cash balance, cash burn. Send all your financials. Refresh and share the cap table. Have a really proactive conversation with a lender.

The lender is going to have to take it to their credit committee and get it approved. But usually a one or two-month thing, they’ll oblige. Now, if you’re looking for something like three to six months, or three to nine months, that’s a whole different ball game. That’s basically treating this deal as a new deal. And oftentimes the lenders will still want to comply because they still want your business, but they’re going to underwrite it in the same way they underwrote your first deal. So they’re going to do some real in-depth due diligence. They’re really going to do a big presentation, their credit committee, and they’re going to probably ask for some compensation in the form of maybe a loan extension fee or some more worth in the company. After all, they’re taking more risk, thus more risk than they originally thought they’re going to take and it’s going to be super important that your company is still executing.

Typically, when the company asks for an extension, it means actually the company is doing well because they don’t really need the money. So that makes the lender want to participate. But if your company is struggling, and you’re asking for two to six months, be prepared for the lender to say no.

If the lender says no on a larger extension, then you can go get another deal put in place or go to your investors and ask for more money.

Interest Only Period

Venture Lenders realize startups want to extend runway and pay back as little of principal as possible. Therefore lenders will grant interest only periods, usually the first 6 to 12 months of a loan, where the startup is only paying interest on the loan. This period is usually timed to end right after a fundraise will take place. The logic is the startup will be flush with equity capital after the fundraise and will be in a position to start paying back the loan.

Investor Abandonment Clause

One of the most ambiguous and dangerous terms in a venture debt agreement. the Investor Abandonment Clause can result in the startup being declared in default of the loan. This term is typically used by a bank to create an event of default if the company is not performing. The venture debt lender can call or email the startup’s investors and ask them to put more money into the company. If the investors decline or don’t follow through with an additional investment to the bank’s satisfaction, the bank can put the company into default and pursue remedies including foreclosure. Banks often say they rarely invoke the Investor Support clause, which is true. However, the bank requires this term so that they can use it or at the very least create leverage. This clause can also create a lot of investor leverage to the Founders detriment because the only way to escape foreclosure is to have insiders write another check.

Lien on Intellectual Property

Lenders has a lien on All the Assets including IP, they can foreclose much quicker because they don’t have to give notice to other creditors. They are the sole beneficiary in a liquidation. Therefore they can foreclose in 10 - 15 days. If the bank had “All Assets except IP,” then it’s more like a 45 - 90 day process.

Material Adverse Change Clause (MAC)

Material Adverse Change clauses are another ambiguous term that lenders use to create an Event of Default. Once a startup is in default, the venture debt lender has tremendous leverage and can pursue remedies like foreclosure. When a lender invokes a MAC, the lender is claiming that something has changed and the borrower will likely not be able to repay the loan. This is an interpretative clause and not a good clause for a startup to agree to. Sometimes Lenders will limit the conditions a MAC can be invoked but we recommend never agreeing to a MAC.

Minimum Cash Requirement in Venture Debt Deals

Banks typically require a minimum cash requirement to reduce their risk. The bank’s goal with this term is to ensure there is adequate cash in the bank account to cover a big portion of the loan if things go poorly. Banks are federally regulated because they loan out other companies’ deposits so they can’t take a lot of risks. The minimum cash requirement limits their risk. This is not a good term for the startup because you’re effectively borrowing your own money and can’t use the capital to extend runway as long as you would like.

An example of a minimum cash requirement is a bank that could provide a $2 million loan, but it requires $1 million to stay in the bank at all times. Therefore the startup only really gets to spend $1 million of the loan extending its runway.

Kruze Consulting aggressively negotiates these out of term sheets whenever possible. If you can’t get it out of your term sheet, then push to reduce the minimum cash requirement as much as possible. Reducing the minimum cash requirement means you are maximizing your runway so you can hit your milestones and raise a big equity round in the future.

Paid Time Off (PTO) Triggering Insolvency

The Board is personally liable for any unpaid employee PTO. When the startup’s cash balance approaches the outstanding PTO balance, a Board will normally admit insolvency and let the lender take control.

Prepayment Penalty

Normally venture debt lenders charge a small pre-payment fee of 1 - 3% of the remaining principal outstanding. If there is a “Final Payment” component of the loan, then that will be due at the time of prepayment as well. Note lenders don’t like pre-payments because only their best companies can afford to pre-pay. Therefore the best credits are refinancing out leaving the lender with less attractive borowers.

Refundable Commitment Fee

Lenders will often ask the Borrower to put down a good faith deposit to ensure the startup is serious about the loan and diligence. Most of the time, the deposit will be credited against the lender’s legal fees.

Springing Lien in a Venture Debt Term Sheet

The supreme lien basically says, ‘Hey, we’re not going to take a lien on intellectual property of the company but if you do get in trouble or hit a go below a cash balance that’s predetermined by the lender, then the lien springs into place and the lender can perfect and actually be confident that they will control that asset.’

Thus, a very common scenario would be maybe a company borrows 5 million dollars of venture debt and the lender says, ‘Hey, as soon as you go under 5 million dollars in cash after you’ve withdrawn our money then we want the lien-in IP to spring into place.’

Before that, ‘Hey, we’re good we don’t need the lien. We trust you.’ But at that moment, that is when the lien is triggered or springs into place. And so, the advantage of this; it’s not a huge advantage to the startup because again when things kind of get bad, the lenders still going to have lien-in IP but it can give the board some comfort and the management team some comfort that the lender won’t always have the lien-in IP and will be a little bit friendlier to deal with until the company hits that predetermined cash balance. Or maybe it’s a revenue covenant something like that.

The lien only comes into play or springs into place when the company triggers some type of covenant that has been predetermined by both the company and lender.

StandStill or Cooling off Period in Venture Debt

This is the legal term but actually, it can have a really huge benefit for a startup.

A cooling off period basically refers to the lender not aggressively foreclosing on the company if they’re in default and where this really comes into play it is if the company has given the lender a lien on the intellectual property and all the other assets.

When that lender has a lien on all assets including actual property they can foreclose very quickly in 10 to 15 days because they don’t have to notify the other creditors who benefit from the sale. If the lender doesn’t have all the assets like a lien on IP they’ll have to notify all the other creditors like the water person or Kruze Consulting or whoever else the company owes money to. That usually takes 60 and 90 days for foreclosure. So, the cooling off period becomes very important.

If the lender has all the assets Lien on IP with the cooling off period says is something to the effect that the lender will not foreclose and sell the company within something like 90 days or 120 days that’s very negotiable as long as the management team is involved and the board is involved and they’re helping to sell the company. What the lender really cares about is if the company actually gets sold and the lender knows that if it’s sold without management team cooperation and board cooperation then they’re going to get ten cents on the dollar. They are going to have a very good recovery. So, what the lender is doing in agreeing to a cooling off here is saying hey as long as you’re playing ball and helping us sell the company helping us get our money back we’re fine not aggressively foreclosing for 90 or 120 days. So, this is a very important term. If you’re giving your lien on IP away to the lender because what you’re basically doing is ensuring as long as you’re engaged as the management team and board you’re not going to get taken advantage of and have a really quick foreclosure.

Now, of course, say you agree in this term in management and just quits and will not help the lender sell the company. Then, of course, the lender is going to move quickly and this term will be thrown out the window.

But I do recommend putting this cooling off period language in a term sheet that you’re giving all the assets of the company with.

Typical Interest Rate on Accounts Receivable Line

Around 4% - 5% is the typical Interest Rate on an Accounts Receivable Line. Note that this is not the All in IRR which is usually around 5% to 6% because of fees.

Typical Interest Rate on Growth Capital Line

Around 9% - 11% is the typical Interest Rate on a Growth Capital Line. Note that this is not the All in IRR which is usually around 11% to 13% on Growth Capital.

Typical Warrant Coverage on an Accounts Receivable Line

Typically Warrant Coverage on an Accounts Receivable Line is 0% to 2% of the total commitment amount.

Typical Warrant Coverage on a Growth Capital Line

Warrant Coverage on a Growth Capital Line is typically 8% to 12% of the total commitment amount. Sometimes a portion of the warrant coverage will be granted upfront and the remaining amount will be granted upon drawdown of the capital.

VC Liquidation Preferences

In Venture Capital, everyone is playing for the home run outcome. However, in a smaller exit, liquidation preferences allow VC’s to get their money back before Common Stock owners, usually Management.

Here is a simple example: A startup raises $4M in Preferred Equity with a 1x liquidation preference. When the company is sold, venture capitalists can choose between receiving their original $4M investment back, or converting to Common and participating with all the other shareholders on a pro-rata basis. If they choose the return of investment, then their investment basically functioned as a loan.

Liquidation preferences are an important tool for VC’s because it mitigates risk. In those scenarios when the startup isn’t a huge exit but does get purchased, the VC’s get their money back and can distribute the capital back to their Limited Partners.

If an investment achieves a big exit, the VC’s will almost always convert, thereby forgoing their liquidation preference, so they can participate alongside other investors and management.

Liquidation preferences are very common in VC investments. Most of the time, VC’s get a 1x preference, but in tough situations, they might ask for 2x or 3x liquidation preference. However, anything more than a 1x is rare.

The essence of a liquidation preference is that VC’s get their money back in a modest exit. In a big exit or an IPO, VC’s will always convert to participate in the big upside.

Venture Debt and the CARES Act

In March of 2020, the Federal Government signed the CARES Act, which is a stimulus bill designed to help small businesses deal with the economic fall out from the COVID crisis. The bill provides one section that may be helpful to startups, the Payroll Protection Program, or PPP. This provides 2.5x monthly payroll in a SBA loan - that is likely to be forgiven if the company keeps headcount and payroll consistent.

There is some confusion if a startup will be eligible for this loan, but assuming that they are, companies that have venture debt need to be aware that the SBA loan needs to be senior to other debt. So these companies may need to go to their lenders asking for permission to bring on debt in a senior position.

Venture Lender's Startup Due Diligence Checklist

All due diligence starts with historical financials. The lender wants to make sure the company has spent its money wisely and can establish a burn rate trend.

Second, lenders want to see future projections. Projections or a Financial Model allow the lender to pinpoint the startup’s cash out date, recognize revenue inflection points, and model out how long the cash infusion will last the company.

Lenders also want to see the cap table so they can see the round prices, especially if the lender is pricing the warrant based on a recent common stock valuation. Understanding the ownership breakdown and which VC’s own how much is important as well. Lenders also like to see the 409A valuation.

Lenders will need an investor presentation as well so they understand the company’s technology, go to market strategy and key performance indicators (KPI’s).

The credit committee will evaluate all these data points, underwrite the deal, and give the startup a term sheet!

Venture Lending Common Events of Default

An event of default is when a startup violates a covenant or does not pay their monthly loan payment. Once a startup is put into Default, the lender controls the companies destiny and can make themselves whole by taking remedies like sweeping cash. A startup should do everything possible to start out of Default. Once in Default, Lenders can make a company fundraise, sell the company or even shutdown. Staying out of default is rule number one.

Rule number two is that a Startup should always insist the Events of Default be in the term sheet. Some lenders get a little sneaky and don’t include the Events of Default in the term sheet. Make the Lenders define the Event of Default before you sign the term sheet so you have the most leverage to negotiate favorable Events of Default. The most common Events of Default are Insolvency or Non-Payment. If you don’t pay your loan, you’re going to be in default. Insolvency is when you don’t have enough money to pay your bills. The Events of Default Startups should be very careful of are Investor Abandonment or Material Adverse Change (MAC). Lenders can use those terms to create a default situation so Startups have to be careful. Regarding an Investor Abandonment Default, the Lender will demand your investors put more money in the company and if the Investors refuse, a default is triggered. Kruze recommends staying away from MAC’s because if there is a big shift in the investment climate or economy, a Lender may try to use a MAC to create a Default. Always try to negotiate a MAC out of your deal. Another lesser-known event of default is when a startup has a material contract breach or it is sued. The Loan Documentation will assign a $ amount threshold where a lawsuit or contract breach becomes a Default. Startups should push for that $ amount threshold to be as high as possible.

If a startup is Series A or B, then that threshold should be a $150,000 to $200,000. The higher threshold means that a small lawsuit of $20,000, will not trigger an event of default.

Warrant Coverage

Venture Debt Lenders ask for equity in the form of warrants to give the lender upside potential on successful companies. This equity component is in addition to the interest rate and final payment. It’s normally quoted as a % of total commitment. As an example, 10% warrant coverage of a $3M loan would be $300k in Warrants. The number of shares in a warrant is derived by the dividing the latest preferred share price into the total $ amount of the warrant. Sometimes lenders will take Common Stock Warrants instead of Preferred Warrants. Do not expect to raise venture debt with out the lender getting warrants, but know that the warrants are going to be much less dilutive than if your startup had raised the same dollar amount of venture capital.

Warrant Coverage Upfront or On Usage

When a lender agrees to a deal, they are committing a million of dollars to the startup. Therefore, they want to get paid both in cash interest and some equity upside via warrants. The lender wants as much equity based committed upfront as possible.

However, the startup wants to preserve as much option value as possible and will ask for the warrant coverage to be based on usage, or the amount drawn down. Often a startup borrower only draws down a portion of the loan so paying all the warrant coverage upfront on committment seems like a waste.

Deals typically end up in the middle with half of the total warrant coming upfront based on commitment and a half on usage. A simple example with easy math is as follows: Warrant Coverage on a venture debt deal is 6% of the total deal amount. About 3% of that would be based on commitment, and 3% on usage. Negotiating warrant coverage to be based on usage can save the startup a lot of unnecessary equity dilution and make venture debt even more attractive.

What Are Prevailing Interest Rate and Warrant Coverage for Venture Debt

In venture debt, you have two types of lenders: banks, and then the fund lenders. So let’s go through the banks first. Banks tend to be a lot cheaper. So right now it’s somewhere between 5 to 7% interest rates.

And then the warrant coverage is also a lot cheaper. Usually, it’s like 1% of the deal amount. Maybe 2% of the deal amount. Usually that kind of equals like .25% of the company’s total ownership.

So banks are much cheaper than fund lenders. Those are the prevailing rates but also remember, banks typically use Investor Abandonment clauses, MAC clauses, other covenants that kinda restrict you a little bit, that’s how they can get away with having lower interest rates and lower warrant coverage.

Now fund lenders, they’re more flexible. They really let you use the money and typically do bigger deals, but they’re more expensive, so fund lenders what I’m seeing these days, is anywhere from 11 to 13% interest rates, that’s on the cash side.

Then the warrant coverage is anywhere from 8 to 12% of the deal amount. So if you’re doing a million-dollar deal, and the warrant coverage is 12%, which is on the high side. But I’m seeing that quite a bit, then that will be a hundred and twenty thousand dollars of warrants in the company, above and beyond what the interest rate cash payments are.

So hope that helps. Again, banks somewhere around 5 to 7% interest rates, 1 to 2% warrant coverage. Funds, anywhere from like 11 to 13% interest rates, and warrant coverage from 8 to 12% of the deal amount.

What is a right of offset

When you take venture debt from a bank, they may ask for a right of offset. Non-bank venture lenders can not ask for this - only a bank that has your checking/savings/money accounts can do it.

- If a bank has an asset (your cash) and a liability (loan out to you) they can offset them against each other

- Dangerous for startups

- Banks only invoke the right of offset if company is in default

- Talk to bank about this before taking a bank loan

What is Venture Debt?

The definition of venture debt (also referred to as venture lending) is a category of debt financing options for early-stage and fast-growing private companies. These securities are created specifically for startups that do not have strong/positive cash flow, and typically are two to four year loans, revenue-based loans or equipment leases.

What to do if you can’t raise Venture Debt?

If you’re trying to raise venture debt, and you can’t do it, that probably means you’re getting a little tight on capital, and so there are some other things you can do to stretch out your company’s runway. The first thing is, there are other lending options, there are revenue-based lenders like Lighter Capital. And they will look at your revenue, give you an advance and then take a portion of that revenue every month, like kind of like four to eight percent of the revenue.

Now it’s expensive money, the IRRs are in the high teens, but it’s a really good option if you’re having trouble raising venture debt. Another thing you can do is go back to your equity investors and see if they’ll do a bridge round.

Now VCs don’t really like to do bridge rounds, but they will do it to support good companies. And really, that’s one of the ways VCs really build their reputations. So it’s worth having the conversation.

Another thing you can do is go to your customers and create a win-win. And you can offer them a discount, you might even want to change your incentive plan for your salespeople a little bit too. Because if you incentivize your salespeople to collect more cash upfront and a lot of times they’ll give the customer a discount to pay upfront, you can actually collect a lot of money.

Often times, companies will sign multi-year deals, and pay the whole thing in advance if the discount is big enough, so that’s a really good one. And finally, if those options aren’t working for you, you may need to cut some burn rate. So, build your financial model. Look at it and look at where your cash goes. And where you’re supposed to hit those milestones.

And if you don’t have enough runway, then that’s the moment where you should make some adjustments. You’re probably gonna have to let some really great people go or maybe not spend money on some really critical vendors. But that’s the trade-off you need to make to extend your runway. So again, you’re going to look at revenue base debt. You’re gonna go back to your VCs for potentially a bridge loan, create some win-wins with your customers to incentivize them to bring cash into the company faster, and you may have to actually cut some burn rate.

Why Do Startups Take Venture Debt?

For startups, Venture Debt functions a lot like Insurance. By taking on incremental capital in the form of Debt, your startup buys itself another three to six months of the runway.

Lenders like to put a debt deal in place when the company raises a new round of equity. So the typical series A or series B startups raise 15-20 months of cash via equity. With debt providing an extra three to six months of runway, the startup has additional room to achieve its milestone and raise its next round at an up valuation.

WTI Prepayment Penalty

WTI is unique in that in the event of a pre-payment, WTI will ask a startup to pay the future interest that would have been paid in future years. There is no discount on future interest for pre-paying a loan. In fact, it’s worse for the startup because the future interest is paid earlier in the loan amortization period so the effective interest rate is actually much higher. Startups typically only do this if they are refinancing into a bigger loan or have raised a lot of equity. Note that because WTI requires the payment of all future interest, the loan is much less attractive to pre-pay. Therefore the borrower is much more likely to stick with WTI and put a larger loan in place rather than refinancing and going with a new lender. WTI’s pre-payment language helps it retain the best borrowers.

Top 6 mistakes companies make when raising venture debt